Thijs Maas

Latest posts by Thijs Maas (see all)

- The Regulation of Cryptocurrencies and ICOs under EU Law - October 3, 2019

- U.S. Regulators want to stop Facebook’s Libra. Here’s why. - July 10, 2019

- The Case for Hybrid Tokens - June 26, 2019

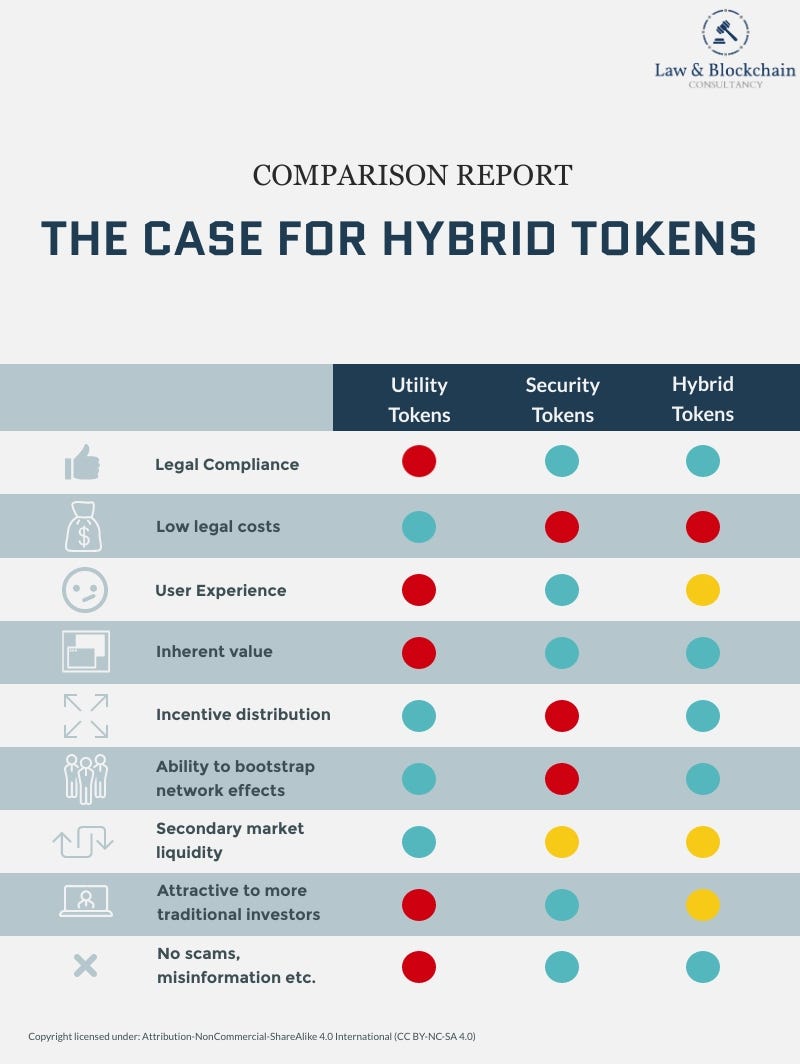

I see many articles proclaiming the death of the Initial Coin Offering. Indeed, volumes of ICO funding have indeed gone down drastically. At the same time, many praise the Security Token Offering (STO) as the ‘next big thing’. The new hype, that will catch people off-guard. However, many misunderstand the differences between ICOs and STO. Even more people underestimate the differences between utility and security tokens. Meanwhile, Hybrid Tokens are mostly ignored… They shouldn’t be. In this post, I will quickly compare utility and security tokens, before making the case that hybrid tokens combine the best of both worlds.

ICOs and Utility Tokens

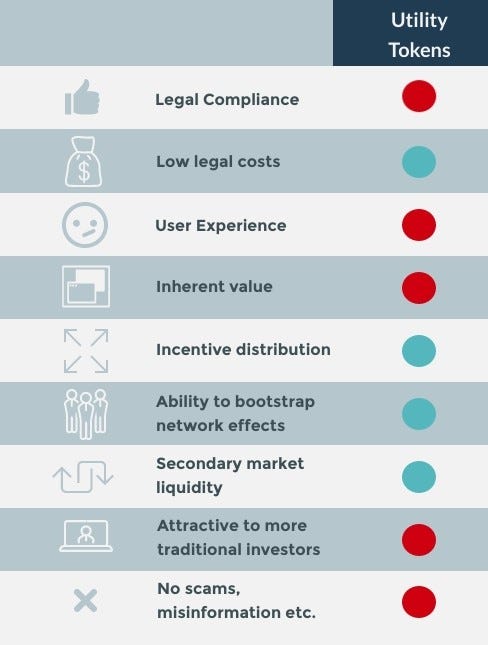

A utility token is a token that is often used as a means of payment for, or access to, a decentralized application, network or service. A predefined amount of tokens is created by an issuer during an initial coin offering, and sold to investors/users. Often, the only way to access any utility (or pay for the goods or services) provided by the corresponding blockchain network, service or decentralized application, is through the issuer’s own token.

Utility tokens are a (very founder friendly) mechanism to raise funding. The strength of utility tokens lies in their ability to bootstrap network adoption. While buying a token early on might not give the investor a lot of utility, this lack of utility is compensated by a large potential for financial gains. After all, a limited amount of tokens is created with no option to create more tokens, which means that if the utility of a protocol/network/application goes up, so should the demand. With the supply staying the same, this should theoretically result in a token’s price appreciation.

Users, advisers, developers and issuers all want to increase the value of the entire ecosystem, as it increases the value of their tokens. Indeed, all parties are incentivized to help build the ecosystem and provide mouth-to-mouth advertising. Any lack of early utility is compensated by an increase in the potential of financial upside. This is important because it helps bootstrap user adoption. A network, protocol or marketplace only has value when other people use it. There’s no point in linkedin if other people don’t use it. There’s no point trying to buy anything on ebay if noone is selling anything. The financial upside given to early users by utility tokens helps solve this chicken-and-egg-problem. [1]

However, the utility token model generally creates a big problem for end-users who are solely interested in using the network’s service: volatility. If I were to, for example, use a decentralized Über-like service, I don’t want to have to hold a token in my wallet that can lose 80% of its value solely because of bad market conditions. If I want to travel tomorrow, I don’t even want the tokens in my wallet to be worth 20% less by then. Volatility makes for a horrible user experience. [2]

The fact every party involved in an ICO profit from a rising token valuation, combined with large information asymmetries, is a problem. The lack of insight into the operations of the issuer, has resulted in a situation where the optimal strategy for an economically rational issuer, who has retained tokens itself, is to (at least in the short term) make people believe there will be a large demand for the token’s utility, instead of actually building a successful dApp, network or ecosystem. They can then profit from the rise in the token’s value. If everyone employs this strategy, a market turns into a marketing shouting contest, with many meaningless ‘strategic innovation partnerships’ and bold claims, which played a large role in the ICO bubble of 2017. It’s one of the main reasons why most ICO companies have never achieved any real adoption.

STOs and security tokens

Due to the problems described above, it makes sense to instead look at different models of token offerings. The security token offering is interesting, as it tackles the main root of the problem with ICOs: the information asymmetries between issuers and investors.

In a security token offering, a token is issued by a project/startup to raise funds as well. However, this token does not act as a scarce resource to unlock future utility. Instead, the security token provides some kind of economic rights to its holders. These can for example take the form of a right to profits or revenues of the issuer. The token could also represent ownership of equities, bonds or other underlying assets.

In short: a security token is not just a bag of hot air based on unproven economic models and hype. Instead, a security token has a more defined degree of inherent value as a result of underlying real-world assets or revenue streams. Investors receive far better information about the issuer and the token offering itself. Moreover, as the security token model is more conservative in its approach, it might prove more attractive to traditional investors, (corporate) VCs and other investors with a lower risk-appetite.

Now one might think that an issuer should just issue security tokens instead of utility tokens. However, security tokens and utility tokens have very different applications. While both are used as a means of fundraising, utility tokens are aimed at creating an ecosystem and means of payment. Security tokens on the other hand can be seen as nothing more than a traditional issuance of economic rights, but now on the blockchain. In other words, STOs and ICOs (generally)have extremely different use-cases.

Compared to ICOs, STOs don’t align incentives between parties as well, and generally don’t bring any significant positive network effects. Security tokens are not as widely distributed accross all parties in an ecosystem, cannot be traded on unregulated markets, and are not used in a blockchain network for utility. Instead, STOs are a mere fundraising technique. Often, it is more fitting to see them as mini-IPO’s for SMEs. They are an alternative or addition to the traditional financing of startups/scale-ups.

Traditionally, a scale-up sells equity in rounds:

- 3F round (friends, family, fools)

- pre-seed

- seed

- post-seed

- Series A

- Series B, C etc.

- Exist through IPO or corporate venture

With every round, more capital is raised. The investors in this model (angels and venture capitalists) are locked in their investment until the IPO or until the company is acquired in some way, which takes 8–12 years. The STO can best be placed somewhere in between the post-seed round(s) and the series A or B, depending on the size of the STO.

The big promise of security tokens is the emerging secondary market for security tokens will provide liquidity for investors. In other words, early investors are not locked in their investments for 8–12 years. Instead, the equity can change hands shortly after the STO. While the ‘liquidity promise’ of STOs could be an impactful evolution in early risk financing, it is still a mere promise. It remains to be seen whether sufficiently liquid and global capital markets will arise. Many parties are currently in a race to provide the required market infrastructure. [4]

Hybrid tokens

As explained, the security token is not a replacement for the utility token: the STO is a completely different model with different applications than the ICO.

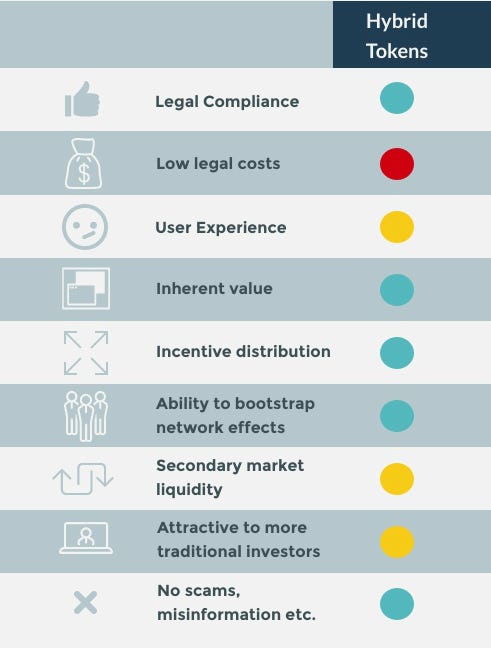

The legal compliance required to issue security tokens ensures that the problems that the ICO market ran into are not applicable to STOs. Issuers are liable for their (mis)statements in the required information disclosure documents, and have to comply with the law. However, the advantages of utility tokens with regards to the alignment of all stakeholders in an ecosystem/network/marketplace are not retained in a security token model.

It therefore makes sense to combine the two models to create a token (offering) structure that leverages the best of both worlds. Introducing: the hybrid token.

Hybrid tokens borrow elements of utility tokens (or even cryptocurrencies). Like with utility tokens, a limited supply is created. These tokens can be used to unlock the utility from a network or decentralized application, thereby acting as a means of exchange within a certain network. Just like with utility tokens, the lack of early utility for token holders in such applications or networks is mitigated by the additional potential for financial gains through the appreciation of a hybrid token’s value when the network becomes more widely adopted.

At the same time however, a hybrid token gives token holders economic rights of some kind. This could for example take the form of additional profit rights or equity rights in the issuer’s business. However, it might also take the form of a right to certain revenue streams within a network.

An interesting example of a hybrid token is the Binance Coin (BNB), which can be used to pay transaction fees on the Binance Exchange. When paying these transaction fees using BNB, the token holder gets a discount on the transaction fees on the exchange. Moreover, the Binance exchange redistributes 20% of its profits to token holders by ‘burning’ BNB tokens, thereby reducing the total supply of tokens, which essentially distributes the value of the burned tokens across all other token holders. [5]

In short, a hybrid token can give equity-like characteristics such as voting rights, dividends and equity ownership as well as retaining the most important characteristic of utility tokens: increased usage of the platform still leads to a direct increase in the token’s price.

So what’s the advantage gained?

Economic rights attached to a hybrid token ensure that more traditional methods of valuation can be applied to figure out the true value of a token. The inclusion of dividends or revenue rights should be more appealing to investors with long-term views, instead of those who are looking for a quick gain. Issuers are meanwhile better incentivized to focus on adoption, as investors are looking for projects with with growing revenues or profit distributions, instead of looking for the most hyped token on social media. This should all result in a reduction of volatility when compared to utility tokens, which improves the user experience for those consumers hesitant to use a volatile instruments to unlock a service or utility.

Most importantly, attaching economic rights to a utility token (resulting in a hybrid token) brings the token offering itself in the realm of securities laws. This means that issuers have to comply with all the requirements usually applicable to the offering of securities (or security tokens). As mentioned earlier, mandatory information disclosures ensure that investors cannot (as easily) be scammed or mislead.

Conclusion

In essence, designing tokens is a balancing act of interests. The utility model is best to tap into excessive market liquidity, to bootstrap a token’s initial adoption and to distribute incentives across all stakeholders of an ecosystem. However, most utility token models are inherently flawed and suffer from the lack of compliance to securities laws.

The security token offering is a fundraising technique with a different use-case. It should be seen as an innovation in the underlying infrastructure for the issuance of financial instruments, which could potentially create more liquid markets for investments that are now illiquid.

Hybrid token models try to combine the best characteristics of both token types. It has the advantages of both utility tokens and security tokens, as incentives are distributed across all actors, while the application of securities laws should get rid of bad actors.

Personally, I would love to see industry move more towards hybrid token models. I am, quite frankly, surprised that hybrid token models have not taken over the market. Of course, there are more costs involved in terms of legal compliance. However, if an issuer can’t cough up the money required to protect its investors, it should probably does not deserve any.

Of course, there are specific legal structures and limited disclosure regimes which can reduce costs, as compared to full registrations or issuance of a prospectus. Through ‘Law and Blockchain Consultancy’ I help companies navigate financial and securities laws and help structure legally compliant token offerings.

[1] Metcalfe’s law states that the effect of a (telecommunications) network is proportional to the square of the number of connected users of the system (n2). This law can be applied to marketplaces, social networks and protocols as well.

[2] The logical thing to do for the consumer would be to only buy the travel-tokens at the moment he intends to spend them on travel, leading to a situation where people don’t actually hold the token. In turn, this leads to the tokens moving around with a ‘high velocity’ within the ecosystem, which in turn increases the volatility. The ease with which the token’s price can be manipulated increases significantly, too. After all, a token which only functions as a medium of exchange can be nudged from one price equilibrium to the next (due to the MV=PQ equation). There are of course a number of ways by which one can increase incentives to hold a token for a longer time without having to venture into the realm of securities laws. See Kyle Samani’s article on token models: https://multicoin.capital/2018/02/13/new-models-utility-tokens/

[3] Exemptions to the issuance of these information disclosures exist. In the US, these are for example Reg CF, Reg D, Reg A(+) and Reg S offerings. The EU’s Prospectus Directive and Regulations similarly have exemptions for e.g. private issuances, offerings to financial institutions and small offerings.

[4] For primary market issuance, see for example Securitize, Harbor, Polymath, Swarm. For secondary market issuance, see tZero, OpenFinance, and the efforts of Gibraltar Stock Exchange, Malta Stock Exchange and Nasdaq’s dx.Exchange.

[5] Even though Binance has not registered any registration statements or prospectuses, the BNB burning scheme largely resembles a share buy-back or dividend distribution. The token would qualify as a security under the US Howey-test, and might be a security in some EU Member States. Even so, BNB has been extremely successful.