Thijs Maas

Latest posts by Thijs Maas (see all)

- The Regulation of Cryptocurrencies and ICOs under EU Law - October 3, 2019

- U.S. Regulators want to stop Facebook’s Libra. Here’s why. - July 10, 2019

- The Case for Hybrid Tokens - June 26, 2019

Ever since Ethereum settled on Switzerland for its Foundation and Initial Coin Offering (ICO), the jurisdiction has been popular among blockchain-based businesses. In fact, the city of Zug is often referred to as ‘crypto-valley’. In this article, I will shortly delve into the laws that apply to ICO’s in Switzerland. Is a Swiss Foundation as smart as it sounds?

The Swiss Financial Market Supervisory Authority (FINMA) recently published guidelines on how it intends to treat ICO’s. FINMA’s CEO, Mark Bransom stated:

“Our balanced approach to handling ICO projects and inquiries allows legitimate innovators to navigate the regulatory landscape and to launch their projects in a way consistent with our laws protecting investors and the integrity of the financial system.”

Like most regulators, each ICO will be examined on its individual merits. In other words, the regulator will look at the economic function and purpose of each individual offering to determine what laws apply. Still, FINMA recognizes the emerging distinction between different kinds of tokens. These are:

- Payment tokens / cryptocurrencies

- Utility tokens: tokens which are intended to provide digital access to an application or service.

- Asset tokens: tokens which represent assets such as participations in real physical underlyings, companies, or earnings streams, or an entitlement to dividends or interest payments. In terms of their economic function, the tokens are analogous to equities, bonds or derivatives.

To make matters slightly more confusing, FINMA states that the individual token classifications are not mutually exclusive. Asset and utility tokens can also be classified as payment tokens (referred to as hybrid tokens). In these cases, the requirements are cumulative; in other words, the tokens are deemed to be both securities and means of payment.

Swiss Securities Regulation

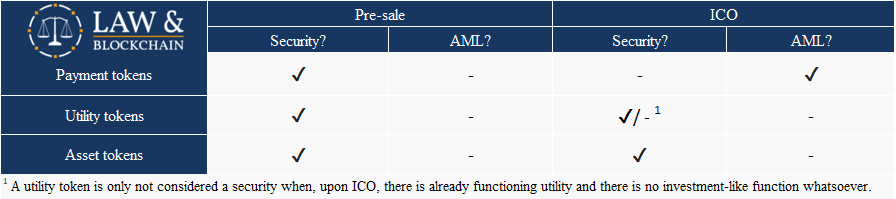

As was to be expected seeing FINMA’s current practice, asset tokens are treated as securities under Swiss securities laws.

Interestingly, FINMA also makes a distinction between pre-sales and ICO’s for payment tokens and utility tokens with a working product or service. Any pre-sale which gives investors a claim to acquire tokens in the future will be treated as securities, no matter what kind of token it is.

ICO’s for utility tokens will generally not be seen as securities offerings. However, there are exceptions to this:

- If, during the ICO of a utility token, there is no working platform or application providing utility to the consumer/investor, the sale is considered a pre-sale, which constitutes the sale of a security.

- If the utility token has any investment-like function whatsoever, the ICO will constitute a sale of a security.

So what if your token is a security under Swiss law?

Well, the regulation of securities in Switzerland is often not as onerous as it is in most other jurisdictions. Under the Swiss Stock Exchange Act, the book-entry and offering of self-issued uncertificated securities is essentially unregulated. However, underwriting or offering securities of third parties will require a licensed under the Swiss Stock Exchange Ordinance. Finally, if the token you are offering is ‘analogous to equities or bonds’, you will most likely also have to satisfy the prospectus requirements of the Swiss Code of Obligations.

Anti-Money Laundering

(i) you provide payment services or

(ii) you issue or manage a means of payment

So, does an ICO automatically make you a ‘financial intermediary’?

No. In fact, only cryptocurrencies / payment tokens will be seen as a means of payment under the AMLA. If you are issuing a payment token, you will have to comply with a number of due diligence requirements. The most important requirements for founders are:

- to establish the identity of the beneficial owner of the buyer (KYC); and

- to affiliate to a self-regulatory organisation or subject yourself directly to FINMA supervision.

For utility tokens, you will likely not be subject to AML-requirements, as long as the your main reason for issuing the tokens is to provide access rights to a non-financial application. For pre-sales, you will never be subject to the AMLA.

The Swiss Foundation

It has become market practice to hold the funds raised during an ICO in a Foundation. Due to the relative legal certainty in Switzerland and low tax-burden, Swiss foundations are often used in this respect. It should be noted however that Swiss foundations are not ideal for this purpose.

First of all, one can only incorporate as a non-profit foundation when the founders do not have any (even indirect) personal financial interest linked to the operation of the non-profit foundation. In many cases, founders retain a small percentage of tokens for themselves, which is something tax authorities might deem a problem.

Secondly, Swiss foundations are by nature very rigid. Swiss law states that these foundations should operate completely independently. Moreover, the money raised during the ICO can only be used for the promotion of the foundation’s purpose.

This is often good news for investors. However, it can also prove to be a burden. The drama of a cryptocurrency called Tezos is a great example hereof.

I will write a full article about the curious tale of Tezos soon. In short, Tezos’ founders, the Breitlings, are dealing with three different US-filed class-actions. Although they successfully raised about $250 million during the ICO, it is still unclear if the funds in the Foundation can be used to cover their legal defense. Is the use of funds for their legal defense for the promotion of the foundation’s purpose? And, as the Breitlings are officially not part of the Foundation themselves, is the Foundation still acting independent if they pay for their defense?

Closing remarks:

- There might be other jurisdictions that are more suitable for your ICO. The relative legal certainty in Switzerland does not always justify doing an ICO there. The Swiss foundation structure is definitely not ideal in most situations.

- FINMA specifically reserves the right to change its mind on payment tokens: ‘if payment tokens were to be classified as securities through new case law or legislation, FINMA would accordingly revise its practice.’

- FINMA considers Ethereum a payment token. While it is true that Ethereum is used to pay miners to execute smart contracts, one might just as well argue that holding Ethereum’s tokens gives access to the platform’s utility. This illustrates that the distinction between payment tokens and utility tokens can be blurry. It could also be that FINMA considers Ethereum a hybrid token.

- Note that compliance with one jurisdiction’s securities/AML/KYC legislation is is only step one. Quite a few regulators have extra-territorial jurisdiction based on nationality!

- None of this is legal advice and you should always consult a lawyer before doing an ICO.

- Get a lawyer

- Seriously, get a lawyer.